What happens day to day in a Factoring operation?

New clients (hopefully), new debtors, new invoices, advances/pre-payments, collections from debtors. All these processes require the systems to do as much of the hard work as possible, leaving the business people to do all the complicated tasks.

New business

First things first, picking the right businesses to become factoring clients is a key to success. Like with many things in life, a factor needs to be able to say “no”. There must be robust processes around vetting potential clients. A factor really needs to understand what they are getting into. Who are the people behind the business? Is the business viable? What is the track record? Lending money is about risk taking, but if an opportunity looks fishy, smells fishy, it probably is fishy, so best to put it back in the sea for someone else to catch!

There is a philosophical position to take here. Many factors are moving towards automated digital processes that make decisions on what businesses to accept and which ones to refuse. Then, there are the more “old school” lenders, who insist upon “kicking the tyres”, visiting the clients’ premises and really understanding the business they may decide to finance. The level of due diligence to apply is about making the right choices. Unfortunately, accepting the wrong clients can prove very costly, but turning away potentially good clients is also unhelpful to a factor’s success. Getting the balance right is crucial.

But what service are we offering?

Factoring has many forms. Is this to be a recourse or non-recourse agreement? Is it for the whole turnover of the business or are we going to offer a selective factoring service and allow the client to just factor certain debtors or even select individual invoices? Will this be a disclosed facility where we notify all the debtors, or will it be confidential, just between us and the client? Are we going to manage the sales ledger on behalf of the client, or will the client continue to manage the collections process?

We can approach the service offering from two sides: what does the business want or need? In other words, what problem are we trying to solve for the business? And from the factor’s position, what can we offer commercially, legally and regarding local market norms? This could be a very narrow product set or a “sweet shop” of a multitude of potential offerings.

The pricing of the deal is an important step.

A client will generate activity and effort that has a cost, and the financing will have a price relative to the risks involved. Traditionally, most pricings break down into service fees and cost of finance. Depending upon the level of servicing required, a classic service fee will be a percentage of the invoice value (plus VAT, in many countries). The cost of finance will be an annual interest rate, probably linked to a base rate. Having said that, factors have been wonderfully skilled at creating many different pricing options, to make the solution work

Once we have identified our client and we have agreed on the commercial terms, the next thing is to have a contract with a set of terms and conditions that are clear and not overly onerous to either party. Traditionally, when it comes to legalities, lawyers seem to love creating tortuous clauses that are mind-blowingly impossible to understand unless you have a large coffee and time to read it several times! Clarity is everything, and many factoring companies are trying to reduce the length of their contracts down to a few important pages rather than hundreds of pages of gobbledegook that must be bewildering, if not terrifying, to the average business person.

We now have our client, a signed contract and we’re all-systems go!

What next?

The first question is where to start? The business was in operation before the signature of the contract, they may well have been factoring with a different factoring company.

For some factors, what happened before the start of the contract is of no interest and it is down to the client (or previous factor) to collect those invoices raised prior to the start of the factoring agreement. Other factoring companies will do a “take-on” and load up the existing debtors and old invoices so that, on day one, they step in to administer the whole sales ledger and act on behalf of the client. Of course, there is likely to be a fee for this take-on service and the factor may or may not choose to advance funds against the taken-on sales ledger position.

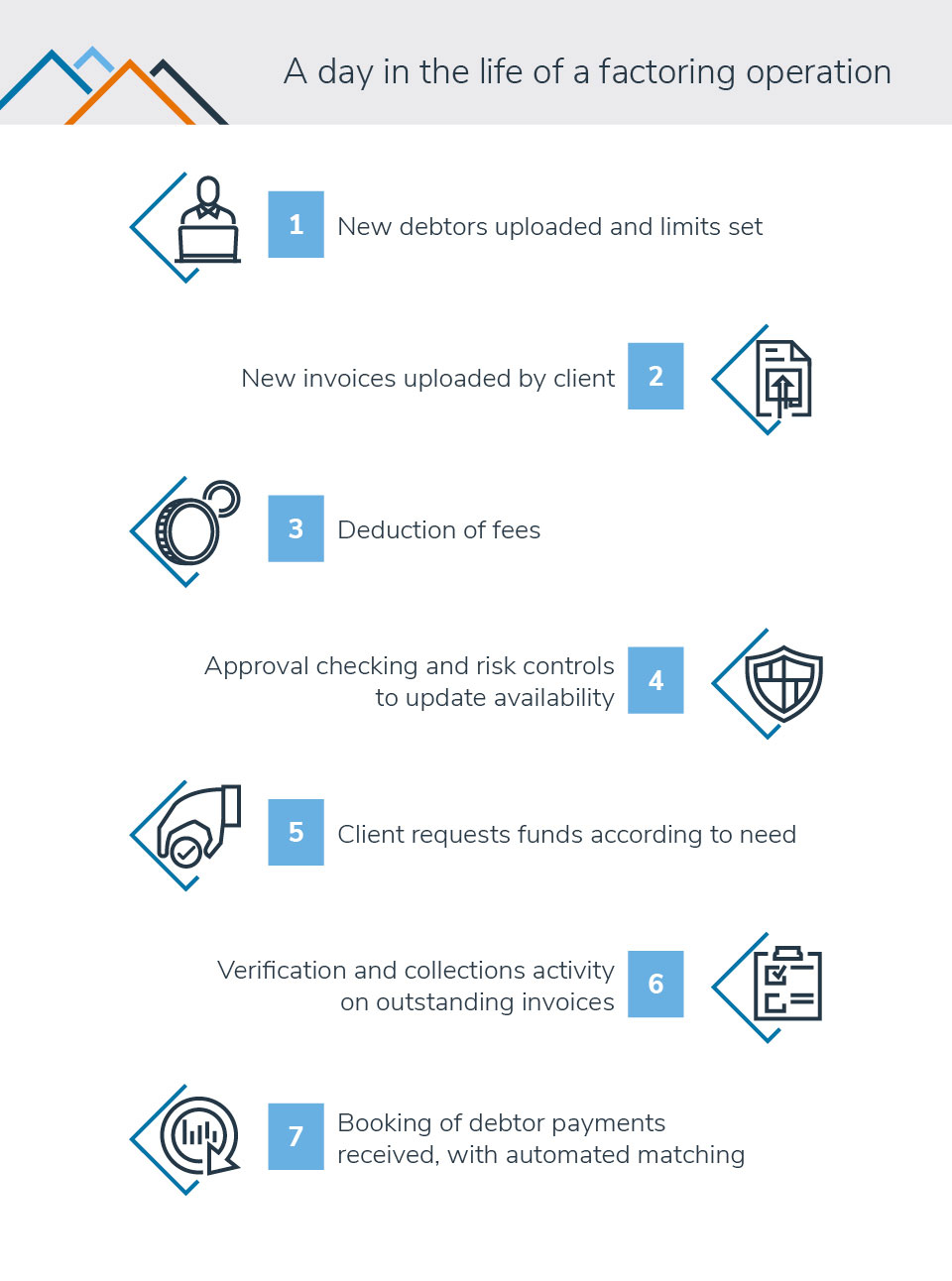

Factoring day-to-day

The day-to-day business of factoring is simple. The client ships goods or provides services and then raises invoices as they would do normally. The invoices are submitted to the factoring company, allowing the client to be financed against the value of the invoice, probably with a percentage retention and deduction of service fees. The factoring company charges interest on the funds in use by the client. On the due date, the debtor pays the factor the full value of the invoice, releasing the retention and paying back the amount advanced. Simple.The flow described above is generally how things work, but there are some processes that the factoring company will probably follow to manage its risk, because it is part of the service or because it benefits the clients.

We’re in a digital world these days and so most factoring companies will offer clients an on-line internet solution. This allows the client to submit new debtors, request credit lines against debtors, submit new invoices and self-service information about their factoring agreement. This not just customer friendly, but also provides huge productivity gains to the factoring company. Some factors will go as far as to offer standard plugins to well-known accounting packages so that the client only needs to raise invoices and for this information to flow automatically from their accounting system to their factoring company.

Invoices arrive at the computer system of the factors (hopefully electronically). Most factors will charge a fee at this point, generally a percentage of the invoice value. The invoice will go through an automated approval process (see Managing Risk below). The approved invoices become part of the Availability against which the client can ask for advances (sometimes called pre-payments).

The availability formula is logically “really” simple, but, as with all things in life, people do like to complicate things! Simple view of availability:

Approved Sales Ledger * Advance % - Funds in Use

In other words, we are going to allow you to have funding against all the good, collectable invoices currently waiting to be paid in your sales ledger (or accounts receivable if you prefer). We might allow 100% to be advanced, but generally the factor likes to keep a bit back, we have fees to be deducted and there may be some invoices that cannot be fully collected. The Funds in Use is effectively the loan balance and is what has already been advanced, but not yet been collected from the debtors.

We told you it was simple. But it can soon become a bit convoluted with additional retentions and reserves or holding back accrued fees and other nuances. But the more complex the formula, the harder it is to explain to the client! Why don’t we just try and keep things simple?

The client requests an amount to be financed, normally within availability, but sometimes over advances may be allowed. This goes through some kind of approval process by the factoring company and if everything is OK, a payment is made to the client. At this point, the Funds in Use is increased, and interest will be charged on this new increased balance daily.

We may impose a limit on the maximum risk exposure that the factor has with a client.

What is the exposure?

If everything went catastrophically wrong, the client and all of the debtors went bust, then the factor would lose the current balance of the Funds in Use, because this is the real money that was advanced, but not repaid. Hopefully, not every debtor would go bust, and the Funds in Use can be fully collected. Anyway, a factor may set a facility limit for the client to keep the FIU below a certain level.

The debtors are encouraged to pay their invoices on the due date using classic credit control/chasing methods. This could be performed by the client or by the factor, as is the case with full-service factoring. In either case, the money collected comes to the factoring company and is credited to the client’s FIU, reducing the balance of the loan. In the case of factoring, allocating the payments to the correct client-debtor relationship (debtor account) and then applying/reconciling the payment to the invoice or invoices being paid can be challenging. This often depends upon what information the debtor provides. Automatic allocation rules can help to reduce the manual effort required.

The FIU goes up and down over the month and interest is typically charged on the daily balance. Interest is normally charged to the client at the end of the month by increasing the FIU by the interest amount. Transactions may be future or back value dated, for example, cheques may be booked, but then take a number of days to clear and become "real money".

Managing risk

But do we fund or purchase every single invoice received from the client? The answer is probably not, as most factors have risk mitigation rules in place, generally automated by their computer systems. At the end of the day, the factor would like to finance everything to provide a good service to the client and earn more fees. However, this is lending money, and so the factor needs to think about the risk of not getting the money back. This falls into three simply categories: (1) can’t pay, (2) won’t pay, (3) nothing to pay!

Working backwards, category three is the worst-case scenario because our client is a fraudster, a criminal, a rotten egg in our otherwise decent portfolio of clients. Prevention is better than the cure, hence why picking the right client is so important. But what other lines of defence does a factor have?

A classic protection is to carry out invoice verification - that is, do something to check that the invoice is a bona fide, good invoice. Generally, this involves contacting the debtor to check that the client is indeed their supplier and that the goods or services were properly delivered, and that the debtor will be delighted to pay the invoice when the due date arrives! Of course, if the debtor has never heard of our client or they have no record of the invoice being received, or there is a problem with the goods or services (not properly) supplied, then we are in trouble, but it’s not too late to do something about it!

What is category one?

This is where a debtor, for one reason or another is unable to pay the invoice. They may still be trading, but on hard times, or they may have completely folded as a business, so we have an out and out bad debt. Again, our first line of defence is before we sign up the client. Scrutiny of the client’s business should extend to its customers. Are they good, reliable businesses or is our client selling to companies that may or may not be around to settle their bills?

The next line of defence is what is often referred to as “disapprovals” or “ineligibles”. Those invoices that the factor (or more likely the factor’s computer system) chooses not to purchase or finance. Firstly, we have the creditworthiness of each of the client’s debtors to consider. Factors may set limits on how much to fund against each one. Some factors will also set concentration limits so that no one debtor is funded above, say 20%, of the total ledger value.

Limits do not stop a client selling to whomever they wish to sell to, but it does help to build up reserves should there be a problem down the line. Other kinds of disapprovals are things like acceptance of old invoices, future dated invoices (which may take us back to category one), disputed invoices (see “won’t pay” below) overdue invoices – anything that may make the invoice uncollectable.

What is category two?

On to category two – “won’t pay”. There are several reasons why a debtor won’t pay. The most common reason is that they were not satisfied by what the client delivered to them, in other words, a good old-fashioned commercial dispute. In this case, the factor simply hands the problem back to the client to resolve and disapproves the invoice as this one may not be collectable.

The client may resolve the dispute by making their customer happy – e.g. replace the faulty goods they had delivered. Or they may reimburse their customer by issuing a refund or a credit note. This is normal in business and not really a major issue to the factor if it happens just now and again. But if the disputed amounts are very large or this is happening on a regular basis, alarm bells should be ringing. This business had probably got some big problems and is heading in a bad direction.

A much more worrying “won’t pay” scenario is if the debtor protests that they have already paid their supplier, our client! This could be a genuine mistake. Accidents do happen. However, this should heighten the factor’s vigilance regarding this client. Did they promptly forward the payment on to the factor? If not, why not? Indeed, did the client inform the debtor to pay them directly and is trying to defraud their factoring company?

Another, different, but similar scenario is where the client is also buying goods or services from the debtor and exercises a right of “offset”. In other words, I won’t pay you “X” because you owe me “Y”, we’ll just offset one against the other and call it quits! Not a good thing from the factoring company’s point of view. This “contra risk” can be identified pre-contract stage, especially as it is more prevalent in certain sectors like haulage. Limits can be used to block funding of debtors that are also suppliers to the client. If all else fails, these invoices will need to be disputed and the client will need to sort out its position with its customer. If the client is agreeing offsetting arrangements with its customers, it should be a clear breach of contract, putting the client on a fast track to termination.

In summary

Factoring enables a company to pay for its operations using the capital it generates from selling off its receivables. There is a reduction in commercial payables for the client, as well as collection time, and improved financial stability.

Article written by: Kevin Day, CEO, Lendscape